The business schedule may be – for some – a little hectic in the middle of summer so now appears a propitious time to examine what can and should be done by wealth advisors to help Baby Boomers get ready for retirement. With all the focus that there has been on what Millennials want, and on issues such as fintech, the US Department of Labor’s Fiduciary Rule, and of course the never-ending political circus over tax, longer-term planning issues aren’t always as potent in grabbing star billing in the headlines. But they are plainly important and a core segment of what wealth management should be about.

With this in mind Diane Harrison, who is principal and owner of Panegyric Marketing, sets out ideas. Her firm is a strategic marketing communications firm founded in 2002 specializing in alternative assets. She is a regulator contributor to these pages. This news service is pleased to share such insights with readers and invites responses. Family Wealth Report does not necessarily endorse all views of guest contributors. Email tom.burroughes@wealthbriefing.com

According to US census figures, Baby Boomers represent about 28 per cent of the US population in 2017, and are currently between 53 and 71 years old. Give or take an error margin of several thousand, this translates to about 76 million people. This significant segment of the population includes both investors and advisors, raising an intriguing question: Just how prepared are we, investors and advisors, for retirement?

First, what are we all thinking?

Insured Retirement Institute’s annual survey report, Boomers Expectations for Retirement 2017, reveals some interesting findings. First published in 2011, the year the leading edge of the boomer generation began to turn 65; the risks identified in the first report remain the same today: Boomers are under-saved, under-planned, have unrealistic expectations, and have an inadequate understanding of the risks they will face in retirement. The full report goes into much detail about the attitudes and expectations of boomers.

Some of the positive findings in 2017 include:

-- Four in 10 boomers believe that selecting investment and insurance products, creating a financial plan for retirement, and planning for health care and long-term care require the help of a financial professional;

-- 85 per cent percent of boomers also said they believe their financial planner is working in their best interest. They believe their advisors are professional and knowledgeable, with the most sought after attributes of a planner being experience and subject matter expertise ; and

-- More than 7 in 10 boomers believe that the compensation their financial advisor receives is fair.

Some of the challenges also revealed:

-- Only 54 per cent of boomers have retirement savings, the lowest recorded in the 7 years of the Boomer report;

-- 82 per cent of boomers underestimate the percentage of their income that may be required to pay for health care;

-- At current savings levels, most boomers with savings face a potential retirement income gap of between $3,864 and $12,072 annually.

Are we prepared for retirement financially?

n large measure, financial advisors struggle with successfully articulating their advisory services in a differentiating way. Universally, advisors bill themselves as a trusted partner, one who offers sound and prudent financial planning for their clients. But what does this mean? And how does that address some of the growing issues boomers are facing as they head into their retirement years?

An unsettling topic was raised in an online article on investopedia.com, 8 Retirement Income Strategies for Boomers in 2017. While the eight strategies covered are typical to most financial plans, these four boomer-related developments are sobering when taken as a whole:

1) Life expectancies are increasing;

2) We are staying active longer;

3) Medical costs for retirees continue to increase; and

4) By many accounts there is a retirement savings crisis in the US.

Traditionally, boomers have relied upon assumptions that a combination of Social Security and their own retirement savings will carry them through their golden years comfortably. But these assumptions have been eroded by a number of developments over the past decades, as persistent anemic interest rates, market meltdowns, real estate bubbles, and regulatory reforms have threatened the underpinnings of these long-held boomer beliefs. Chuck Saletta wrote in a February article on retirement, 3 Bold Predictions for 2017, that Social Security's trust funds remain on track to run out of money around 2034, slashing benefits for all recipients by more than 20 per cent. Retirement planners should consider the risks of either that kind of reduction in Social Security, or the potential of an equivalent tax hike to cover its costs.

Advisors are challenged by these issues and others as they try to deliver coherent and long-term financial solutions to an under-prepared aging boomer population. What’s an advisor to do? You’ve no doubt heard the saying ‘you can’t teach an old dog new tricks.’ It seems the aging boomer generation needs to embrace new thinking and advisors need to retool traditional planning techniques to help bridge the financial retirement dilemma. There won’t be a generalized, one-solution-fits-all approach that will serve this large and increasingly complex segment of the coming retirement population.

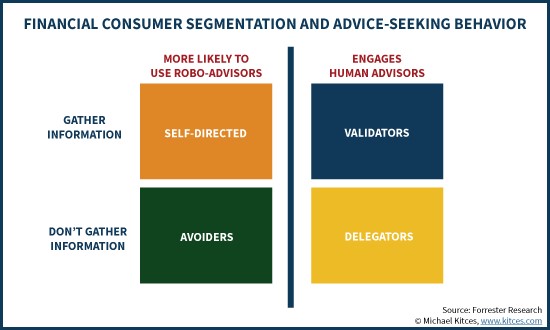

he looming impact of health care costs and services will influence retirement funds and planning, and with no clear solution on the horizon for how healthcare services and costs will be managed in the US, advisors and consumers are left guessing how best to prepare for the coming years. Boomers are also showing their independent thinking in how they view financial planning services. Some will try to go it alone, relying on information and self-directed techniques to solve their individual needs, while others will continue to seek the advice and support of the professional community to put together comprehensive plans that achieve overall financial goals.

As the following graphic demonstrates, the boomer generation is segmenting themselves as they tackle retirement issues.

Source: Forrester Research © Michael Kitces, www.kitces.com

For of those to whom much is given, much is required - Luke 12:48

Boomers have long been in the trend-setting vanguard of the past half century, with their population dominance shaping the growth of many sectors of the US economy. As the boomers begin to exit the workforce and enter the retirement phase of their lifespan, they will undoubtedly continue to exert outsize influence on the general population.

Financial advisors will need to adapt their services and approaches to keep up with this segment in ways that are focused on these large-scale needs. Advisors particularly need to align their financial planning tools with the murky waters of healthcare costs. There will be little to guide advisors as healthcare struggles to accommodate such a significant demand on services that boomers create. Compounding this issue will be the complexities of a global financial dance that US interest rate policy continually seeks to navigate. Advisors have a daunting role to fill but a large client population to serve for those who are up to the challenge.

About the author

Diane Harrison is principal and owner of Panegyric Marketing, a strategic marketing communications firm founded in 2002 specializing in alternative assets. She has over 25 years’ of expertise in hedge fund and private equity marketing, investor relations, articles, white papers, blog posts, and other thought leadership deliverables. Her firm has won multiple industry awards. A published author and speaker, Ms. Harrison’s work has appeared in many industry publications, both in print and online.